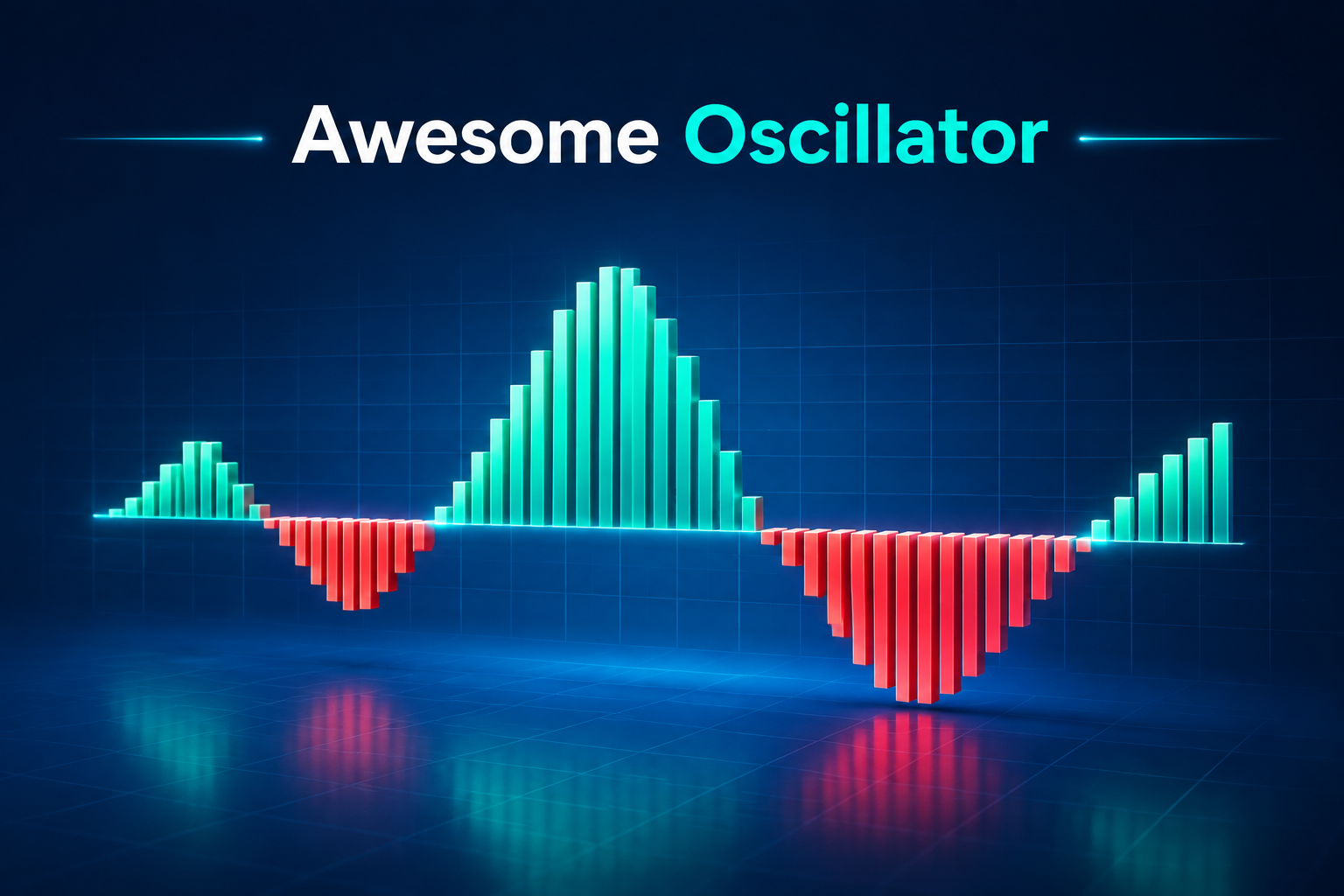

An Awesome Oscillator strategy helps traders assess market momentum by comparing recent price movement with a longer-term momentum baseline. The indicator appears as a histogram around a zero line, showing whether momentum is strengthening, weakening, or changing direction. This Evest guide explains how the Awesome Oscillator works, its standard 5-period and 34-period SMA settings, and key signals such as zero-line crossovers, Saucer formations, Twin Peaks, and divergence. It also highlights that AO should not predict prices alone. Every signal should be confirmed with price action, market structure, support and resistance, volatility, and risk-management rules.

What Is the Awesome Oscillator Indicator?

The Awesome Oscillator indicator measures the difference between short-term and longer-term momentum. It compares a 5-period simple moving average with a 34-period simple moving average, calculated from each bar’s midpoint rather than its closing price.

The result appears as a histogram in a separate window below the price chart. Values above zero mean the 5-period average is higher than the 34-period average, while values below zero mean it is lower.

A green bar normally means the current AO value is higher than the previous value, while a red bar means it is lower. These colours describe changes in the indicator, not guaranteed changes in price. A green bar does not automatically mean that the market will rise, and a red bar does not automatically mean that it will fall.

AO is best treated as a momentum-measurement tool rather than a standalone market prediction.

How Does the Awesome Oscillator Work?

AO compares recent momentum with a broader momentum baseline. When the 5-period average rises above the 34-period average, the histogram moves into positive territory. When the shorter average falls below the longer average, the histogram moves into negative territory.

The distance from the zero line also matters. Expanding bars may suggest that the difference between the two averages is increasing, while shrinking bars may suggest that the difference is narrowing.

However, the size of the histogram alone does not provide an entry point. Traders still need to consider trend direction, support and resistance, volatility, and the structure of the price chart.

Because AO is calculated from moving averages, it reacts to price data that has already been recorded. This makes it a lagging indicator. Its value lies in organising momentum information and highlighting changes that may deserve closer analysis.

How Is the Awesome Oscillator Calculated?

The calculation starts with the midpoint of each price bar:

Median Price = (High + Low) ÷ 2

The indicator then calculates two simple moving averages:

AO = 5-Period SMA of Median Price − 34-Period SMA of Median Price

A positive AO value means the recent 5-period average is above the longer 34-period average. A negative value means the recent average is below it.

Simple Calculation Example

Assume AO is being calculated at the close of candle 34. At that same point:

- The 5-period SMA uses the midpoint prices of candles 30 to 34 and equals 1.0870.

- The 34-period SMA uses the midpoint prices of candles 1 to 34 and equals 1.0800.

- The calculation is AO = 1.0870 − 1.0800 = 0.0070.

- The positive result shows that the recent average is above the longer average.

Both moving averages must end at the same candle. Comparing averages that end at different points would not represent the AO value for one specific moment.

Best Awesome Oscillator Settings

The standard Awesome Oscillator settings use a 5-period SMA and a 34-period SMA, both calculated from the midpoint of each bar. These values form the original Bill Williams calculation and are the appropriate starting point for most users.

In Evest’s trading environment, users can focus on how the histogram behaves around the zero line while keeping the standard calculation based on 5 and 34 periods. A version that uses different periods should be treated as a customised indicator rather than the default AO.

The chart timeframe does not change the 5/34 formula. It changes the duration represented by each bar. On a 15-minute chart, the 5-period average uses five 15-minute bars. On a daily chart, it uses five daily bars.

There is no universally best timeframe. Shorter charts can produce more signals but also more market noise. Higher timeframes tend to produce fewer signals and may offer clearer market structure. The right choice depends on the trader’s holding period, the asset being analysed, and the testing results.

How to Use Awesome Oscillator Trading Signals?

The main Awesome Oscillator trading signals are the zero-line crossover, the Saucer setup, and Twin Peaks. Traders may also monitor divergence between price and the histogram.

A practical Awesome Oscillator strategy should not treat these patterns as automatic buy or sell instructions. Before acting on a signal, traders should check the wider trend, nearby support and resistance, current volatility, and whether price action confirms the change in momentum.

A structured process can include the following steps:

- Identify whether the market is trending or moving sideways.

- Check whether AO is above or below the zero line.

- Look for one clearly formed signal.

- Confirm the setup using price structure or another relevant tool.

- Define the entry, invalidation level, and position risk.

- Avoid entering when the expected reward does not justify the risk.

- Record the outcome for later review.

Zero-Line Crossover

A zero-line crossover occurs when AO moves from negative to positive territory or from positive to negative territory. A move above zero shows that the 5-period average has risen above the 34-period average. A move below zero shows that the shorter average has fallen below the longer average.

This reflects a shift in momentum, but it does not confirm that a sustained trend has started. When using a crossover as part of an awesome oscillator strategy, traders should look for confirmation from the price chart.

Examples include a breakout from a defined range, a higher high in an existing uptrend, a lower low in an existing downtrend, or a reaction from a recognised support or resistance level.

Crossovers are less reliable in sideways markets. AO may repeatedly move above and below zero without price developing a lasting direction. This can lead to late entries and repeated losses if every crossover is traded.

Example Bullish Checklist

A bullish crossover setup may be stronger when the wider price structure is bullish or has clearly shifted upward, AO crosses from below zero to above zero, price closes above a relevant resistance level or forms a higher high, the stop location is based on price structure rather than the AO window, and the potential reward is acceptable relative to the planned risk.

Saucer Signal

The Saucer is generally treated as a momentum-continuation setup. A bullish Saucer forms above the zero line when two consecutive declining bars are followed by a rising bar. In the standard colour display, this often appears as two red bars followed by a green bar.

A bearish Saucer is the opposite formation below the zero line: two rising bars followed by a declining bar. The setup should only be considered complete after the third bar forms.

The position of the pattern relative to the zero line is important. A bullish Saucer belongs above zero, while a bearish Saucer belongs below zero. Within an awesome oscillator strategy, the Saucer is more relevant when it agrees with the existing market direction.

A bullish formation against a strong downtrend, or directly below major resistance, deserves more caution. Traders should also avoid anticipating the third bar before it closes, because the colour and shape can change while the candle is still forming.

Twin Peaks

Twin Peaks is used to identify a possible loss of momentum before a reversal or a stronger correction. A bullish Twin Peaks setup forms below the zero line. AO creates two downward troughs, with the second trough closer to zero than the first.

The histogram must remain below zero between the two troughs. This pattern suggests that negative momentum may be weakening.

A bearish Twin Peaks setup forms above the zero line. The second upward peak is lower and closer to zero than the first, while the histogram remains above zero between the peaks. This may indicate that positive momentum is weakening.

Twin Peaks does not guarantee a reversal. Price can continue in the same direction even after the second peak forms. When this setup is included in an awesome oscillator strategy, confirmation can come from a break of structure, a rejection candle, or a reaction from a significant price level.

Awesome Oscillator Divergence

Awesome oscillator divergence occurs when price and AO form opposing patterns. Bullish divergence appears when price records a lower low while AO forms a higher low. This may indicate that bearish momentum is weakening.

Bearish divergence appears when price records a higher high while AO forms a lower high, which may indicate that bullish momentum is weakening.

The most important point is that divergence is an early warning, not a completed reversal signal. Price can continue moving in its original direction for an extended period after divergence appears. Entering immediately can expose the trader to further movement against the position.

When awesome oscillator divergence is used within an awesome oscillator strategy, traders should wait for confirmation. This may include:

- A trend-line break.

- A change in swing structure.

- A reversal pattern.

- A clear response from support or resistance.

Divergence is also easier to interpret when the two price swings and the two AO swings are clearly defined. Forcing a divergence between minor or unrelated points can create a signal that is not objectively repeatable.

Combining AO With Price Action and Other Tools

AO becomes more useful when every tool has a specific role. The indicator can measure momentum, while the price chart provides context and defines the invalidation level.

- A moving average may help identify trend direction. Support and resistance can highlight areas where a signal is more or less meaningful. Volume, where reliable volume data is available, may help assess participation during a breakout.

- Using several indicators that all measure similar information can create unnecessary complexity. For example, combining multiple momentum oscillators may produce repeated versions of the same signal rather than independent confirmation.

- A simple framework is often more practical. The trend filter can be based on market structure or one moving average, the momentum signal can come from AO, the entry trigger can be a breakout, rejection, or candle close, and risk control should rely on a stop based on price structure and predetermined position size.

The purpose of confirmation is not to remove all losing trades. No combination can do that. Its purpose is to create consistent conditions that can be tested and repeated.

Choosing a Timeframe

The timeframe should match the trading plan. Short-term traders may analyse lower timeframes, but these charts contain more noise, spread impact, and rapid signal changes.

Swing traders may prefer four-hour or daily charts because the market structure is often easier to define. A trader can also use a higher timeframe for direction and a lower timeframe for entry timing.

Changing the timeframe should not be used to search for a signal that confirms an existing opinion. The analysis process should define in advance which timeframe provides the trend context and which timeframe, if any, provides the entry.

The same signal can behave differently across assets and market conditions. A setup that appeared effective during a trending period may perform poorly during a range. Historical testing should therefore include different volatility environments.

Using the Awesome Oscillator With Evest

Evest users can use the Awesome Oscillator as part of a structured technical analysis process focused on momentum, price confirmation, and risk control.

Clients using Evest can open an asset chart, review the available technical tools, and apply AO-based analysis according to the trading plan. After adding the indicator, select the asset and timeframe defined in the trading plan.

Monitor the zero line, histogram direction, and the specific setup being tested. The built-in charting tools can be used alongside price levels, market structure, and risk-management planning.

The presence of an indicator signal should not be treated as a recommendation to open or close a position. Before making a decision, traders should assess the wider trend, volatility, support and resistance, position size, and individual risk tolerance.

A demo environment can be used to practise the platform process and test clearly defined rules without placing live capital at risk. Simulated results can still differ from live execution and should not be treated as a guarantee.

Common Mistakes to Avoid

A strong awesome oscillator strategy should avoid common interpretation errors. AO can help organise momentum information, but traders still need clear rules, price confirmation, and disciplined risk control before using any signal as part of a trading plan.

1- Trading Every Colour Change: A change from red to green only means the latest AO value is higher than the previous value. It does not automatically create a complete signal.

2- Ignoring the Zero Line: The location of a Saucer or Twin Peaks pattern relative to zero is part of the formation. Removing that condition changes the setup.

3- Entering Before the Candle Closes: Histogram bars can change while the price candle is still active. Waiting for the selected candle to close creates a more consistent rule.

4- Using AO Without Market Context: A momentum signal directly into major resistance or support may have limited room to develop. The price chart should remain the main source of context.

5- Placing a Stop at the AO Zero Line: The indicator’s zero line is not a tradable price. Stops need to be linked to price structure and position risk.

6- Changing Settings Without Testing: Custom values may make the histogram react faster or slower, but that does not mean performance improves. Any customised version needs separate testing.

FAQs

What Are the Standard Awesome Oscillator Settings?

The standard Awesome Oscillator settings use a 5-period SMA and a 34-period SMA, calculated from each bar’s median price. These values form the original calculation. Visual preferences may vary, but alternative periods should be treated as customised settings and tested separately.

What Are the Main Awesome Oscillator Trading Signals?

The main Awesome Oscillator trading signals are the zero-line crossover, Saucer, Twin Peaks, and divergence. Each signal has specific conditions and should not be treated as a guaranteed entry or exit. Traders should confirm signals with price action, structure, and risk rules.

Which Timeframe Is Best for AO?

There is no single best timeframe for AO. Lower timeframes may produce more signals but more noise, while higher timeframes usually offer fewer signals and clearer structure. The right timeframe depends on the trader’s holding period, asset, and testing results.

How Should Traders Interpret Awesome Oscillator Divergence?

Awesome oscillator divergence may suggest that momentum behind the current price move is weakening. Bullish divergence appears when price makes a lower low while AO makes a higher low. Bearish divergence is the opposite. Confirmation is still required because divergence can persist.

Can AO Be Used by Itself?

AO can be read independently, but using it alone removes important market context. Price structure, trend direction, support and resistance, volatility, and risk management help traders decide whether a momentum signal is relevant enough to include in a trading plan.

Can AO Be Used for Different Asset Classes?

The Awesome Oscillator can be applied to different price charts available on Evest. However, signal behaviour may vary because assets differ in liquidity, volatility, trading hours, and transaction costs. Each market and timeframe should be tested separately before relying on any setup.