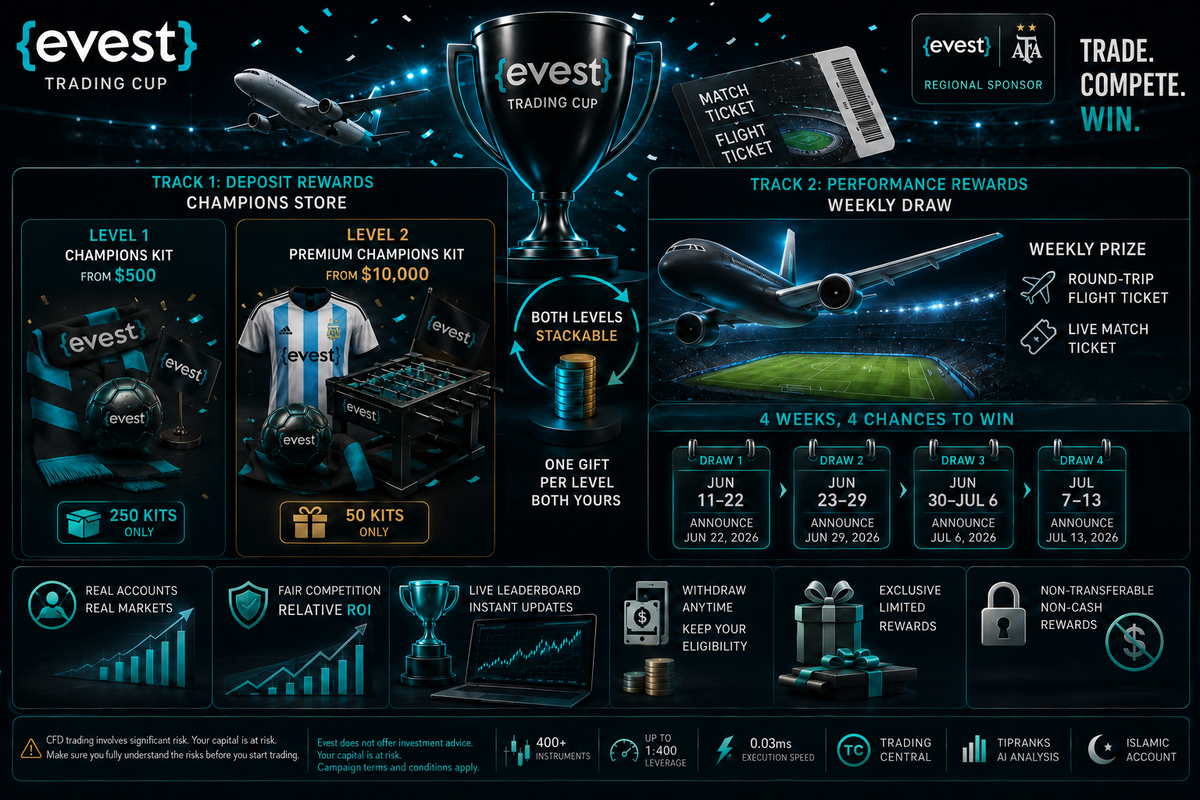

Evest Trading Cup Rewards — Champion-Level Rewards

What makes a trader dedicate their full focus and strategy to a single competition? The answer is always the Evest Trading Cup rewards — prizes that go beyond mere numbers to become a real experience and an unforgettable memory. Evest designed this season’s reward structure with exceptional care, combining instant deposit-based rewards with performance-based weekly prizes — ensuring every serious trader finds their place in the winners’ circle. Whether you’re looking for an exclusive kit that captures the spirit of the season or dreaming of a live match ticket on the stadium floor, the Evest Trading Cup rewards are built to give every trader exactly what they deserve.

Trading Cup Reward Structure — A Complete Overview

Trading Cup rewards from Evest are split into two fully independent tracks — you can qualify for one or both simultaneously:

Evest offers two distinct reward types this season, and that’s precisely what makes the Trading Cup reward distribution more comprehensive and fair than any other trading competition on the market.

The Two Reward Tracks

- Track One — Deposit-Based Rewards (Champions Store) Granted automatically the moment you hit the qualifying deposit threshold — no competition, no ranking required. Just deposit and qualify.

- Track Two — Performance-Based Prizes (Weekly Draw) Awarded to the trader with the highest ROI during each weekly draw period.

Champion Kits — Exclusive Champions Store Rewards

Champion kits are the most prominent Evest rewards for traders on the deposit-based track, split into two levels based on qualifying deposit size during the campaign period.

Level 1 — Champions Kit

Available to every trader who makes a single transaction of $500 or more between June 11 and July 19, 2026.

Kit contents:

- Official fan scarf

- Evest-branded football

- Your favourite team’s flag

Only 250 kits available — strictly limited quantity.

Level 2 — Premium Champions Kit

Available to every trader whose cumulative deposits reach $10,000 or more during the campaign period.

Kit contents:

- Official fan scarf

- Evest-branded football

- Official Argentina national team jersey

- Your favourite team’s flag

- Evest-branded foosball table

Only 50 kits available — extremely limited.

The Two-Level Stacking Rule

One point many traders overlook: the two levels are not mutually exclusive. If you start with a $500 deposit and claim the Level 1 kit, then grow your cumulative deposits to $10,000 later in the campaign, you qualify for the Level 2 kit on top of the first — one gift per level, both yours to keep.

Weekly Trading Competition Prizes — The Weekly Draw

The biggest trading competition prizes in the Evest Cup are those awarded through the performance-based weekly draw. Four draws, four prizes, and four opportunities that don’t repeat.

Weekly Draw Prize

In each draw, the trader with the highest ROI percentage wins:

- Round-trip economy flight ticket to the match city

- One live match ticket to watch the champions on the pitch

Weekly Draw Schedule

| Draw | Period | Announcement Date |

| Draw 1 | Jun 11 → Jun 22, 2026 | June 22, 2026 |

| Draw 2 | Through Jun 29, 2026 | June 29, 2026 |

| Draw 3 | Through Jul 6, 2026 | July 6, 2026 |

| Draw 4 | Through Jul 13, 2026 | July 13, 2026 |

Types of Trading Cup Rewards — Full Comparison

To fully understand the types of Trading Cup rewards, here’s the complete side-by-side comparison:

| Criterion | Champions Store | Weekly Draw |

| Qualification basis | Deposit size | Highest ROI |

| Number of winners | Everyone who meets the threshold | One trader per week |

| Prize type | Exclusive sports kit | Flight + match ticket |

| Quantity available | 250 + 50 kits | 4 prizes across the season |

| Stackable | Yes — two levels | No — one win per trader |

| Withdrawal impact | Does not cancel eligibility | ROI calculated at draw date |

Winning Trader Rewards — Claiming Conditions

Winning trader rewards in the Evest Cup are subject to a set of conditions every participant should know:

- Non-transferable: Prizes cannot be passed to another person under any circumstances

- Non-redeemable for cash: All rewards are physical and cannot be converted to account credit or monetary value

- Subject to verification: Submitting a claim does not guarantee delivery until Evest confirms all eligibility conditions are fully met

- Claim process: Via the dedicated claim form at champion evest, with full contact and shipping details required

Why Evest Trading Cup Rewards Are Exceptional?

Evest rewards for traders aren’t just financial incentives — they’re a complete experience that reflects Evest’s philosophy as the official regional sponsor of the Argentine national team. Here’s what makes them stand apart:

- Priceless emotional value: A live match ticket is a memory that lasts for years — not a number that disappears into your account balance

- Exclusive limited-edition kit: Only 250 + 50 kits for an entire season — scarcity that gives them exceptional collector value

- A reward for every level: Not just the top performer — everyone who meets the deposit threshold gets their own dedicated reward

- Full transparency: The live leaderboard shows you at every moment exactly where you stand relative to the biggest prize

CFD trading involves significant risk. Your capital is at risk. Make sure you fully understand the risks before you start trading.

FAQs

Can I get a Champions Kit and a weekly draw prize at the same time?

Yes — the two prizes are completely independent. If you deposit $500 and claim the Level 1 kit, then achieve the highest ROI in a weekly draw, you receive the kit and the flight and match ticket together. The system is designed to reward the committed trader on more than one level simultaneously, and that's what makes the Trading Cup rewards from Evest structurally unique compared to any other trading competition.

Will my prize be affected if I withdraw funds during the campaign?

No. Withdrawals do not cancel prizes you have already earned. If you qualified for the Champions Kit with a $500 deposit and then withdrew part of your funds, your right to the kit remains fully intact. For the weekly draw, your return is calculated based on your portfolio value at the draw date relative to your total deposits — so a withdrawal affects the calculated ROI percentage, not your fundamental eligibility.

How long does it take to receive Champions Store rewards?

Delivery timelines depend on logistical arrangements and third-party shipping providers, and may vary by country and service provider. Evest contacts winners to request shipping details after eligibility is confirmed. For direct enquiries, reach out via the official campaign email: [email protected]

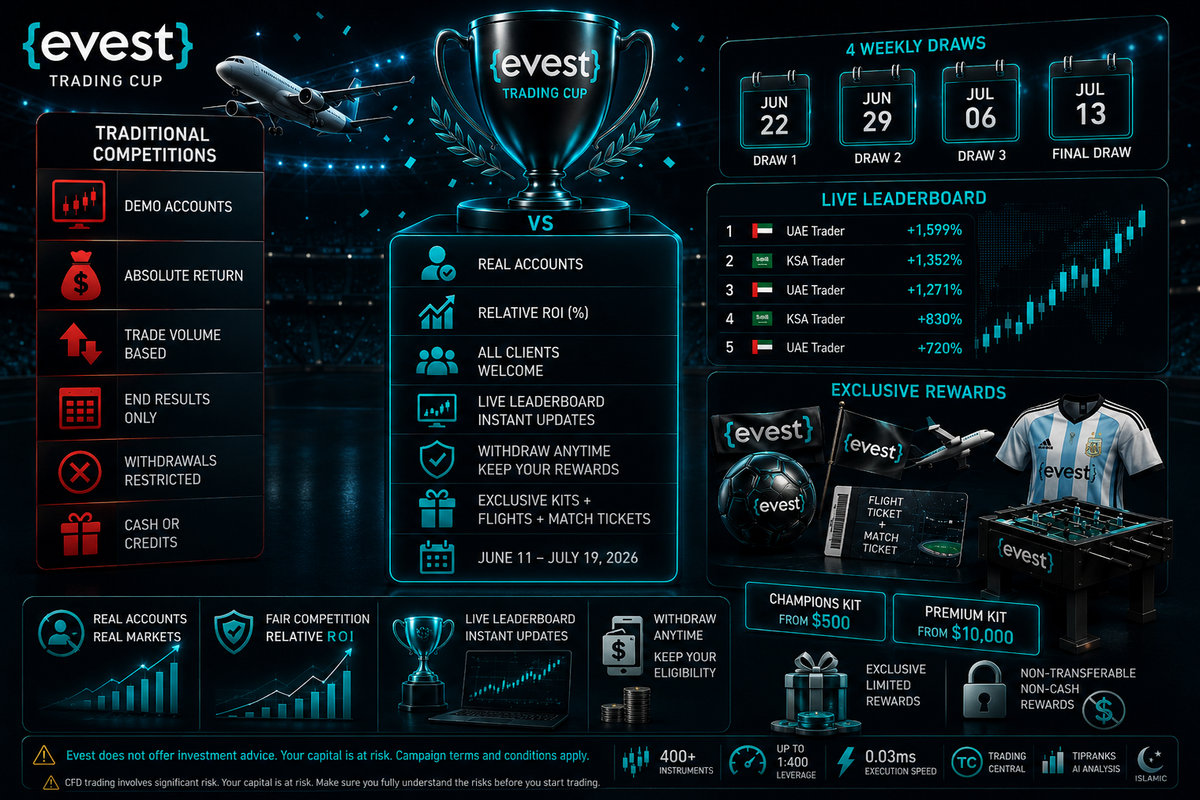

Trading Cup vs Trading Contest: What’s the Difference?

Not all trading competitions are the same — and if you’ve ever participated in regular trading competitions before, you’ll immediately recognise that the gap between a Trading Cup vs trading contest is far wider than most traders expect. The Evest Trading Cup operates on an entirely different level — the difference isn’t just in prize size or competition duration, but in the complete philosophy the tournament is built on, from the scoring mechanism, to eligibility conditions, to the nature of rewards, all the way through to the overall experience a trader lives throughout the season. If you’re wondering why everyone is talking about the Evest Cup this summer, this article gives you the full answer.

Types of Trading Competitions — Understanding the Landscape

Before diving into the comparison, it’s important to understand the types of trading competitions available in the market so you can place the Evest Trading Cup in its proper context.

The Most Common Models in Trading Competitions

- Demo Account Contests The most widespread format in the market — participants compete on virtual accounts with simulated money. No real risk, but no real value in winning either. The winner is often whoever took the most exaggerated risks, precisely because the money isn’t real.

- Absolute Return Competitions Whoever generates the largest gain in dollars wins — automatically giving traders with large accounts an unfair structural advantage over smaller participants, regardless of actual trading skill.

- Trade Volume Competitions These reward whoever opens the highest number of trades — encouraging random trading over strategic thinking, and often benefiting the broker far more than the trader.

- Classic Global Trading Tournaments Typically organised on large platforms over extended periods, relying on complex criteria that don’t suit the everyday trader and often lack transparency throughout the competition window.

Trading Tournament vs Trading Competition — Where the Real Difference Lies

Trading tournament vs trading competition — the difference in terminology reflects a genuine difference in substance. A competition is a passing event. A tournament is a complete experience with structure, philosophy, and prizes that match the level of ambition it demands.

| Criterion | Regular Trading Competition | Evest Trading Cup |

| Basis of competition | Absolute return or trade volume | Relative ROI (Return on Investment) |

| Account type | Demo account in most cases | Fully live and real |

| Eligibility | Sometimes restricted | All new and existing clients |

| Prizes | Cash or trading credit | Exclusive kits + flights + match tickets |

| Transparency | Limited leaderboard | Live leaderboard updated instantly |

| Withdrawals | End of competition only | Permitted at any time |

| Duration | Days or weeks | June 11 → July 19, 2026 |

| Cultural connection | None | Official AFA Argentina partnership |

What Makes the Trading Cup Different — The Real Advantages?

What makes the Trading Cup different from everything else isn’t just bigger prizes — it’s a complete system of advantages that make the experience deeper, fairer, and more exciting than any traditional trading competition.

1. Real Account Competition — Not a Demo

The most fundamental difference between the Evest Cup and traditional trading challenges is that every single trade in the Cup is executed with real money in a real market. This means:

- Decisions are calculated because real capital is on the line

- Genuine skill determines the winner — not luck or reckless risk-taking

- Winning means proving actual trading competence against a live global market

2. A Formula That’s Fair for Everyone — Relative Return, Not Absolute

In regular trading competitions built on absolute returns, a trader with $50,000 automatically outperforms a trader with $500 — even if the smaller trader is significantly more skilled. The Evest Trading Cup eliminates this disparity entirely through the relative ROI formula. Everyone competes on the same ground, regardless of account size.

The formula is straightforward:

ROI (%) = ((Portfolio value at draw date − Deposits during campaign) ÷ Deposits during campaign) × 100

A $500 deposit achieving +300% outranks a $50,000 deposit achieving +15% — every single time.

3. A Live, Fully Transparent Leaderboard

Classic global trading tournaments typically announce results only at the very end — keeping participants in the dark throughout the entire competition period. The Evest Trading Cup operates with complete transparency:

- The leaderboard updates instantly at champion evest

- Your ranking is visible to you and all participants at every moment

- You can adjust your strategy in real time based on where you currently stand

4. Four Weekly Draws — Renewed Opportunities Every Week

Most regular trading competitions produce a single winner at the very end. The Evest Trading Cup gives you four separate chances to win through consecutive weekly draws:

- June 22, 2026 — First Draw

- June 29, 2026 — Second Draw

- July 6, 2026 — Third Draw

- July 13, 2026 — Fourth and Final Draw

And if you win one draw, you’re excluded from subsequent ones — opening the door for more traders to claim a prize across the season.

5. Complete Freedom to Withdraw

One of the standout Trading Cup advantages that’s absent from most other competitions is that withdrawing your funds doesn’t cancel your eligibility. You can withdraw at any point during the campaign without losing the rewards you’ve already earned — a level of flexibility that’s extremely rare in traditional trading competition formats.

Trading Cup Advantages — What You Won’t Find Anywhere Else

The Trading Cup advantages go well beyond the competitive structure to deliver a complete experience with no equivalent:

- Prizes That Can’t Be Measured in Numbers A round-trip flight ticket and a live match ticket aren’t money that disappears — they’re a memory that stays. This category of prize simply doesn’t exist in any standard trading competition format.

- Official AFA Argentina Partnership The Evest Cup isn’t just a trading competition — it’s a seasonal event tied to Evest’s official partnership with the Argentine Football Association (AFA). This connection gives the Cup an exceptional character that bridges the world of financial markets with the spirit of global football championships.

- Exclusive Champions Store Alongside the weekly draw prizes, the Cup rewards your deposit directly through the Champions Store — giving every qualifying participant a tangible, exclusive seasonal kit regardless of their leaderboard position.

- A Complete Trading Platform The competition runs on the Evest platform equipped with 400+ financial instruments, leverage up to 1:400, order execution at 0.03ms, and advanced analytical tools including Trading Central and TipRanks — everything a professional trader needs in one place.

CFD trading involves significant risk. Your capital is at risk. Make sure you fully understand the risks before you start trading.

FAQs

Why does the Trading Cup use live accounts instead of demo accounts?

Because real competition requires real stakes. On demo accounts, traders tend to make exaggerated decisions precisely because nothing is at risk — which makes the results a poor measure of actual trading skill. The Evest Cup selects traders who prove their competence under real market conditions, which is what makes winning it a genuine achievement that demonstrates measurable, recognisable trading ability.

Can I join the Trading Cup without any previous experience in trading competitions?

Absolutely. The Evest Cup requires no history in global trading tournaments or previous competitions. All you need is an active Evest account, completed KYC verification, and a deposit of $500 or more during the campaign period. The platform also offers the Trading Academy and expert webinars with Ahmed Osama to help new traders build a strong foundation before and during the competition.

What's the real difference between Trading Cup prizes and prizes from other trading competitions?

Most traditional trading challenges offer cash prizes or additional account credit — rewards that disappear with the next trade. The Evest Trading Cup goes in a completely different direction: a flight and a live match ticket are an experience that can't be valued in dollars, and the exclusive Champions Kits are limited-edition seasonal pieces. The goal of this choice is for the memory of winning the Cup to stay with you — not dissolve into the daily movement of the markets.

How Does Hidden Divergence Work?

Hidden divergence is a signal that occurs when the relationship between price action and a momentum indicator suggests that the current trend is about to resume after a pullback or consolidation phase. Unlike regular divergence, which signals potential reversals, hidden divergence is a continuation signal. It tells you that the underlying momentum driving a trend remains intact even when the price has temporarily moved against that trend, and that the market is likely to resume its primary direction with renewed force.

What is Hidden Divergence?

The concept of hidden divergence sits within the broader family of divergence analysis, which compares the behavior of price to the behavior of a momentum indicator to identify situations where the two are telling different stories. Understanding where hidden divergence sits within this family, and why it is distinct from its more widely known counterpart, is the essential starting point.

Regular divergence, the type most traders learn first, occurs when the price makes a new high or low that is not confirmed by the momentum indicator. Price reaches higher, but momentum is actually weakening. This is a reversal warning. Hidden divergence is the opposite scenario. The momentum indicator makes a new extreme that is not matched by a corresponding new extreme in price. Momentum is showing strength that the price has not yet fully reflected. This is a continuation signal.

The distinction matters enormously for how you use the signal. A trader who confuses regular divergence with hidden divergence will be looking for reversals when the market is actually setting up for a powerful trend continuation move, which is one of the most costly analytical errors in trend trading.

How Does Hidden Divergence Work?

- Momentum measurement: Hidden divergence is considered a reliable signal because it reflects what the momentum indicator is actually measuring beneath the surface of price movement.

- Pullback within an uptrend: When price pulls back during an uptrend but the momentum indicator stays above its previous comparable low, it suggests that buying pressure has not weakened in the same way price has.

- Shallow momentum correction: Even if the pullback looks significant on the price chart, the momentum decline may be relatively shallow, indicating that the trend still has underlying strength.

- Healthy trend correction: This type of divergence often signals a normal correction within a healthy trend rather than the beginning of a full reversal.

- Institutional participation: Markets showing hidden divergence during pullbacks are often supported by continued institutional activity or sustained dominant market flow.

- Temporary pullback: The price decline may be caused by profit-taking or short-term sentiment changes, while the main trend direction remains intact.

- Objective confirmation: Hidden divergence gives traders a measurable way to assess trend strength instead of relying only on subjective market analysis.

- Trend continuation signal: Because the dominant buying or selling pressure remains present, hidden divergence is often used as a continuation signal rather than a reversal signal.

Bullish Hidden Divergence: Finding the Entry Point Within an Uptrend

Bullish hidden divergence is the variation of the signal that appears within an established uptrend and signals that the trend is ready to resume after a corrective pullback. It is formed by a specific relationship between price and the momentum indicator that, once you know what to look for, becomes recognizable on almost any chart where a genuine uptrend is underway.

The setup forms when price makes a higher low during a pullback within an uptrend. This is the key price action condition. Price has corrected, but the correction has held above the previous significant low, confirming that the higher low structure of the uptrend is intact. Meanwhile, the momentum indicator makes a lower low during the same pullback period. The indicator has dropped further than the price has, suggesting that the surface appearance of the correction is slightly more pessimistic than the underlying market reality warrants.

This combination, a higher low in price with a lower low in the indicator, is bullish hidden divergence. It tells you that the correction is complete, that the sellers who drove the pullback have not been strong enough to undermine the trend’s foundation, and that the conditions are in place for upward momentum to reassert itself.

How to Identify and Confirm Bullish Hidden Divergence?

Follow this process to identify valid bullish hidden divergence setups on your charts.

- Confirm that the market is in an established uptrend by identifying a series of higher highs and higher lows on the time frame you are analyzing.

- Wait for a corrective pullback that forms a new higher low, meaning it does not break below the prior significant low.

- Check your momentum indicator at the corresponding point of the pullback low.

- If the indicator is showing a lower reading at this higher low in price than it showed at the prior swing low in price, you have bullish hidden divergence.

- Look for confirmation from price action, such as a reversal candlestick pattern, a break of short-term resistance, or a return to momentum in the indicator, before entering.

- Place your stop below the higher low that formed the divergence, as a break of that level would invalidate the continuation setup.

Bearish Hidden Divergence

Bearish hidden divergence is the mirror image of the bullish variation, appearing within an established downtrend to signal that the trend is resuming after an upward correction. It is equally powerful as a signal and equally important to understand, particularly for traders who are comfortable taking short positions or trading instruments that allow profit from falling prices.

The setup forms when price makes a lower high during an upward correction within a downtrend. This confirms that the corrective bounce has not broken the downtrend’s structure of lower highs and lower lows. At the same time, the momentum indicator makes a higher high during the same corrective period. The indicator is showing more apparent strength than the price is reflecting, but within the context of a downtrend, this is actually a bearish signal because it confirms that the correction is exhausting itself before it can genuinely challenge the prevailing trend.

This combination, a lower high in price with a higher high in the indicator, is bearish hidden divergence. It signals that sellers are likely to regain control and drive prices lower in continuation of the dominant downtrend.

RSI Hidden Divergence

The RSI, or Relative Strength Index, is one of the most widely used momentum indicators in technical analysis and one of the most effective tools for identifying hidden divergence. Developed by J. Welles Wilder and introduced in 1978, the RSI measures the speed and magnitude of price movements on a scale from zero to one hundred, with readings above seventy traditionally considered overbought and readings below thirty considered oversold.

For hidden divergence analysis, however, the absolute level of the RSI matters less than the relationship between successive RSI readings at equivalent points in the price cycle. You are not looking for overbought or oversold conditions. You are comparing where the RSI stands at a current price swing low or high relative to where it stood at the previous equivalent swing point.

Practical RSI Settings for Hidden Divergence Analysis

The standard RSI period setting of 14 is a reasonable starting point for most time frames, but hidden divergence analysis benefits from some flexibility in this setting.

| Time Frame | Recommended RSI Period | Rationale |

| Daily and Weekly Charts | 14 periods | Standard setting works well for longer cycles |

| 4-Hour Charts | 14 periods | Standard setting appropriate for swing trading |

| 1-Hour Charts | 10 to 14 periods | A slightly shorter period increases sensitivity |

| 15-Minute Charts | 7 to 10 periods | A shorter period better captures intraday momentum shifts |

| 5-Minute Charts | 5 to 7 periods | A very short period was needed to capture fast-moving signals |

Regardless of the period you use, the method for identifying RSI hidden divergence remains identical. Compare the RSI reading at successive swing lows during uptrends or successive swing highs during downtrends and look for the divergence between the RSI reading and the corresponding price level.

MACD Hidden Divergence

The MACD, or Moving Average Convergence Divergence indicator, provides another powerful lens through which to identify hidden divergence. The MACD measures the relationship between two exponential moving averages of price and presents this relationship as both a line and a histogram, making it visually intuitive for divergence analysis.

MACD hidden divergence follows the same basic logic as RSI hidden divergence, but uses the MACD line or histogram to identify the momentum condition. In a bullish hidden divergence setup, price makes a higher low while the MACD histogram makes a lower low or the MACD line makes a lower reading than it did at the prior swing low. In a bearish setup, price makes a lower high while the MACD shows a higher reading than it did at the prior swing high.

One of the advantages of using the MACD for hidden divergence analysis is that the histogram makes the divergence visually prominent. The shrinking or growing bars of the histogram at successive swing points create a clear visual representation of whether momentum is expanding or contracting relative to the price being shown.

Why Hidden Divergence Is the Trend Trader’s Best Friend?

- Primary application: Trend continuation is the primary application and the primary benefit of hidden divergence analysis.

- Established trends: For traders who operate primarily within the context of established trends, identifying high-probability re-entry points after corrective moves is one of the most valuable skills available.

- Trend trading challenge: Even strong, well-established trends do not move in straight lines.

- Corrective phases: Trends advance and retreat, with corrective phases that can be psychologically difficult to navigate.

- Corrections and reversals: Corrections look like reversals until they prove not to be.

- Common trader mistake: Many traders exit winning trend positions during normal corrections only to watch the trend resume without them.

- Hidden divergence solution: Hidden divergence provides an objective, indicator-based signal that a correction is ending and that the trend is resuming.

- Trading application: Rather than exiting the trend during the correction or waiting for a new trend high to confirm resumption, the hidden divergence trader can identify the likely end of the correction before it happens and position accordingly.

The Advantage of Trend Continuation Signals Over Reversal Signals

Trading with the trend using continuation signals rather than against it using reversal signals offers several practical advantages.

- Higher probability of success because you are aligned with the dominant market direction

- More favorable risk-to-reward ratios because stops can be placed at the correction low or high, which is a defined and logical level

- Reduced exposure to false signals because the broader trend context filters out many low-quality setups

- More consistent results over time because trend continuation setups occur repeatedly within any sustained trend

Momentum Indicators: Choosing the Right Tool for Your Analysis

While RSI and MACD are the most commonly used momentum indicators for hidden divergence analysis, they are not the only options available. Understanding the strengths and limitations of different momentum tools helps you choose the right one for your specific trading style and the markets you analyze.

The Stochastic Oscillator is another popular choice for hidden divergence analysis. Like the RSI, it operates on a bounded scale and provides clear visual reference points for comparing momentum at successive swing levels. The Stochastic tends to be more sensitive than the RSI, which makes it useful for shorter time frame analysis, but also means it generates more noise that requires filtering.

The Commodity Channel Index, or CCI, operates on an unbounded scale and measures the deviation of price from its statistical mean. Some traders prefer it for hidden divergence because its unbounded nature means extreme readings carry more information than the capped readings of bounded oscillators like RSI.

Regardless of which indicator you choose, the key principles remain the same. You are always comparing the indicator reading at a current price swing point to the reading at the prior equivalent swing point, and you are looking for a divergence between what price is doing and what the indicator is doing that reveals information about underlying momentum.

Building a Complete Hidden Divergence Trading System

Hidden divergence is most powerful when it is integrated into a complete trading system rather than used in isolation. A complete system built around hidden divergence signals typically incorporates the following elements working together.

- Trend identification comes first. Before looking for any hidden divergence setup, confirm the direction and strength of the prevailing trend on the time frame above the one you plan to trade. This provides the context that distinguishes a genuine continuation signal from a false setup.

- Signal identification comes next. Apply your chosen momentum indicator to your trading time frame and scan for the specific price and indicator conditions that define bullish or bearish hidden divergence at current market swing points.

- Confirmation is the third element. Rather than entering immediately on the divergence signal, wait for price action confirmation that the correction is ending. This can take the form of a bullish or bearish reversal candlestick, a break above short-term resistance in a bullish setup, or a break below short-term support in a bearish setup.

Entry and risk management complete the system. Enter the trade after confirmation with a clearly defined stop loss placed at the level that would invalidate the divergence setup, typically just beyond the correction low in a bullish setup or the correction high in a bearish setup. Define your profit target based on the prior swing high or low, a key resistance or support level, or a fixed risk-to-reward ratio.

How Hidden Divergence Performs Across Different Market Conditions?

- Best market condition: Hidden divergence performs best in trending markets where a clear price structure makes it easy to identify valid higher lows and lower highs during corrections.

- Weak market condition: In ranging or choppy markets, the signal loses much of its effectiveness because there is no dominant trend direction to provide the context that gives the signal its meaning.

- Market environment assessment: Assessing the market environment before applying hidden divergence analysis is as important as the analysis itself.

- Suitable trending market: A market that has been trending clearly for weeks or months on a daily chart is a far more suitable environment for hidden divergence trading.

- Unsuitable ranging market: A market that has been moving sideways within a range for an extended period is less suitable for hidden divergence analysis.

- Higher time frame structure: The best markets for hidden divergence analysis show clean, defined structure on the higher time frame.

- Clear swings and momentum: These markets have clear swing highs and lows, consistent momentum in the direction of the trend, and proportionate corrections.

- Deep correction risk: Corrections should not be so deep that they effectively negate the existing structure.

- Best market examples: Forex major pairs, liquid equity indices, and major commodity markets typically provide the cleanest environments for this type of analysis.

FAQs

What is the difference between regular divergence and hidden divergence, and how do I know which one I am looking at?

Regular divergence occurs when price makes a new extreme in its current direction, but the momentum indicator fails to confirm that new extreme, signaling that momentum is weakening and a potential reversal may follow. Hidden divergence is the opposite: the momentum indicator makes a new extreme that price does not confirm, signaling that momentum is stronger than the price action alone suggests and that the current trend is likely to continue. The easiest way to remember the difference is by what each type signals.

Can hidden divergence be used effectively on all time frames and all asset types?

Hidden divergence is a universal concept that applies across all time frames and all liquid financial markets, including forex, equities, commodities, and cryptocurrencies. The signal works on a five-minute chart for intraday traders and on a weekly chart for long-term position traders, using the same identification logic in each case. The key variable is that the quality of the signal generally improves as the time frame increases, because higher time frame signals represent larger and more meaningful moves in momentum and are less susceptible to short-term noise.

How many confirmations should I wait for before entering a hidden divergence trade?

The appropriate number of confirmations depends on your trading style and risk tolerance, but at a minimum, you should always wait for at least one form of price action confirmation before entering a hidden divergence trade. Taking a trade purely on the divergence signal before the price has shown any sign of the correction ending is a common mistake that leads to entering too early and being stopped out by continued corrective moves before the trend resumes.

Does the Trading Cup depend on account size?

The question on every trader’s mind before joining the Evest tournament is: Does the Trading Cup depend on account size? And is the trader with the biggest balance always the one who wins? The short answer is no — and that’s precisely what makes this tournament different from any other trading competition out there. The Evest Trading Cup is built on a relative Return on Investment formula, not on the absolute value of returns, placing small and large traders on the same competitive ground. In other words, what determines your position on the global leaderboard is how smart your decisions are — not how big your portfolio is.

How Does the Trading Cup Calculate Rankings?

To understand the impact of account size on trading results in the Cup, you first need to understand the core formula the system runs on:

ROI (%) = ((Portfolio value at draw date − Deposits during campaign) ÷ Deposits during campaign) × 100

This formula says one thing clearly: the percentage is everything — the absolute number is irrelevant.

A Practical Example That Makes It Clear

| Trader | Deposit | Gain | Return | Ranking |

| A | $500 | $1,500 | +300% | First |

| B | $10,000 | $8,000 | +80% | Second |

| C | $50,000 | $20,000 | +40% | Third |

Trader A deposited the least of all — yet leads the leaderboard by a wide margin. This is the essence of the relative return in the Trading Cup — percentage always outranks size, without exception.

Does Capital Affect the Trading Cup?

Account size in the Trading Cup does have an influence — but not in the way most people imagine. Let’s break this down precisely.

What Account Size Does NOT Affect?

- Your leaderboard ranking: The formula is entirely relative and gives no advantage to larger accounts

- Your eligibility for the weekly draw: The only requirement is a $500+ deposit during the campaign — regardless of your total account balance

- Your right to claim Champions Store rewards: Tied to your qualifying deposit amount, not your overall account size

What a Larger Account Does Provide?

- Greater flexibility margin: A larger account absorbs market volatility more comfortably without hitting a margin call

- Ability to diversify positions: Opening multiple positions across different instruments simultaneously

- Premium Kit eligibility: A $10,000+ cumulative deposit unlocks Level 2 of the Champions Store

Can You Win With a Small Account?

Yes — and the Draw 1 leaderboard figures prove it. The top performer achieved +1,599% — and that extraordinary return doesn’t require a massive account. It requires a solid strategy, precise timing, and smart use of the tools available on the Evest platform.

Why a Small Account Can Compete at the Highest Level?

- Leverage compensates for the capital gap: Evest offers leverage up to 1:400 on foreign currencies, giving a trader with $500 a purchasing power of up to $200,000

- Focus outperforms diversification: A trader with a small account concentrates carefully on one or two positions — and that focus is itself a competitive advantage.

- The formula rewards efficiency, not wealth: $500 achieving +500% beats $50,000 achieving +10% — always and without exception.

Minimum Account Size in the Trading Cup

The trading account in the Trading Cup requires no large balance to get started. The minimum for full participation and eligibility is straightforward:

- $500 single deposit during the campaign period to enter the weekly draw and unlock the base Champions Kit

- $10,000 cumulative to qualify for the Premium Kit and the full Champions Store package

The minimum account size in the Trading Cup is $500 — a real starting point, not an intimidating figure. Evest set this threshold deliberately because the Cup’s philosophy is built on democratic competition: the opportunity belongs to everyone, and the top belongs to whoever earns it.

Does the Deposit Affect Trader Ranking?

Does the deposit affect trader rankings on the leaderboard directly? The answer: not directly — but it has an indirect effect worth understanding:

- A higher deposit reduces your potential return rate if absolute gains are equal, so depositing more means you need to achieve proportionally higher gains to maintain the same percentage

- A lower deposit amplifies the impact of every absolute gain on the final rate, which works in favour of the careful trader with a modest account

- In the event of a tie in ROI, the trader with the highest absolute gain wins — and this is the only moment where deposit size directly influences the outcome

Trading Cup and Capital Size — The Definitive Summary

Trading Cup and capital size are not linked factors — and that’s the real beauty in how this tournament is designed. Here’s what to keep in mind:

- The competition is entirely relative — ROI percentage is the only metric that matters

- $500 is enough to enter a genuine contest for the biggest prizes

- Evest’s leverage compensates for capital differences between traders

- Strategy and timing always outperform size in the Cup’s formula

- Does winning depend on capital? The definitive answer: winning depends on your decisions — not your portfolio

CFD trading involves significant risk. Your capital is at risk. Make sure you fully understand the risks before you start trading.

FAQs

Does the trader with the bigger account always beat the smaller trader in the Cup?

No — and the formula structurally prevents it. The relative ROI system makes every trader compete against themselves first: how much were you able to grow what you deposited? A trader with $500 who achieves +400% outranks a trader with $100,000 who achieves +50% — and this isn't an exception in the Cup. It's the foundational rule that the entire competition was built on from day one.

Can I increase my deposit mid-campaign to improve my chances?

Yes, you can deposit at any point during the campaign running from June 11 to July 19, 2026. However, keep in mind that every additional deposit enters the denominator of the ROI formula — meaning you'll need to achieve proportionally higher returns to maintain the same percentage. Additional deposits are useful for qualifying for the Level 2 Champions Store reward ($10,000 cumulative), but they require adjusting your trading strategy to match the new capital size accordingly.

What's the real difference between depositing $500 and depositing $5,000 in the context of the Cup?

The core difference isn't eligibility — both qualify for the weekly draw and the Level 1 Champions Store reward. The difference is in flexibility margin: the trader with $5,000 has a larger safety buffer protecting them from market volatility and the freedom to open multiple diversified positions. But at the end of the day, the leaderboard doesn't see absolute numbers — it sees percentages only, and that's the sole determinant of your ranking.

Cross currency pairs: what they are and how to trade them?

Cross currency pairs represent a sophisticated yet accessible segment of the foreign exchange market, offering traders exposure to economic dynamics beyond the dominance of the US dollar. Unlike major currency pairs, these pairs exclude the USD entirely, allowing investors to capitalize on regional trends, political developments, and interest rate differentials between non-USD currencies. In 2026, understanding cross currency pairs is essential for diversifying portfolios and exploiting unique market opportunities. This guide explores their types, trading strategies, and the key factors driving their volatility, providing actionable insights for both beginners and experienced traders.

Types of Currency Pairs in Forex Trading

In the world of Forex trading, currency pairs are broadly categorized into three types: major pairs, cross currency pairs, and exotic pairs. Each category serves distinct purposes and appeals to different trading strategies.

- Major currency pairs, such as EUR/USD or USD/JPY, dominate the market due to their high liquidity and tight spreads. These pairs are directly tied to the US dollar, making them sensitive to global economic trends and USD strength.

- Cross currency pairs, however, involve currencies that do not include the USD, such as EUR/GBP or EUR/JPY. These pairs reflect the economic relationship between two non-USD currencies, offering exposure to regional economic conditions. For example, EUR/JPY captures the interplay between the Eurozone’s economic policies and Japan’s monetary stability.

- Exotic currency pairs, like USD/TRY or EUR/ZAR, involve currencies from emerging markets. While these pairs offer higher volatility potential, they are typically less liquid and come with wider spreads, making them riskier but potentially more rewarding for traders seeking speculative opportunities.

How Cross Currency Pairs Differ from Major Pairs?

Cross currency pairs differ from major pairs in several critical ways, primarily due to their indirect relationship with the USD and the economic fundamentals of the currencies involved.

- Base and Quote Currency Dynamics: In cross currency pairs, both currencies are non-USD. For instance, in EUR/GBP, the euro is the base currency, and the British pound is the quote currency. This structure means the pair’s movement is influenced by the economic policies and conditions of both the Eurozone and the UK, rather than just one major economy tied to the USD.

- Liquidity and Volatility: Major pairs like EUR/USD benefit from high liquidity, resulting in tighter spreads and lower transaction costs. Cross currency pairs, however, often exhibit higher volatility due to their indirect relationship with the USD and the economic disparities between the two currencies. For example, EUR/JPY can experience significant price swings during periods of uncertainty in either the Eurozone or Japan, leading to wider spreads and more pronounced price movements.

- Economic Drivers: Cross currency pairs are highly sensitive to regional economic indicators. For example, EUR/GBP is influenced by Brexit developments, ECB policies, and the UK’s economic outlook. Similarly, GBP/JPY reflects the volatility of the British pound combined with the stability of the Japanese yen, making it attractive for traders seeking high-risk, high-reward opportunities.

How Cross Currency Pair Prices Are Actually Calculated?

Most traders accept the quoted price of a cross currency pair without questioning how that price is derived. Understanding the actual calculation mechanism, however, gives you a meaningful edge in spotting pricing inefficiencies and understanding why spreads on cross pairs tend to be wider than on major pairs. The answer lies in the fact that virtually all cross currency pair prices are calculated indirectly through the US dollar, even though the dollar does not appear in the pair itself.

The Cross Rate Calculation in Practice

When you see a price quoted for EUR/GBP, that price is not determined independently. It is derived by dividing the EUR/USD rate by the GBP/USD rate. If EUR/USD is trading at 1.0800 and GBP/USD is trading at 1.2600, the derived EUR/GBP rate is 1.0800 divided by 1.2600, which gives approximately 0.8571.

This indirect calculation has a direct practical consequence for traders. Because the cross rate is derived from two separate major pairs, any spread or pricing imprecision in either of those pairs feeds into the cross rate. The result is that cross currency pairs almost always carry wider bid-ask spreads than the major pairs from which they are derived, and any slippage in execution on a cross pair is effectively the combined slippage risk of two simultaneous major pair transactions. Understanding this mechanism helps you evaluate the true cost of trading a cross pair versus trading the underlying major pairs separately, and it explains why cross pairs generally require larger price moves to cover transaction costs compared to major pairs.

Top Cross Currency Pairs to Trade in 2026

In 2026, several cross currency pairs stand out for their liquidity, trading volume, and potential for profit. These pairs are favored by traders for their responsiveness to economic news and geopolitical events.

- EUR/GBP: Known as the “Chunnel” pair, EUR/GBP is one of the most liquid cross currency pairs. Its movement is heavily influenced by Brexit-related developments, European Central Bank (ECB) policies, and the UK’s economic outlook. Traders often use this pair to gauge the relative strength of the euro against the pound, making it ideal for those focused on European economic trends.

- EUR/JPY: This pair, often referred to as the “Yen Cross,” reflects the strength of the euro against the safe-haven Japanese yen. It tends to rally during global uncertainty, as investors flock to the yen for safety. EUR/JPY is particularly sensitive to interest rate differentials between the ECB and the Bank of Japan.

- GBP/JPY: Combining the volatility of the British pound with the stability of the Japanese yen, GBP/JPY is attractive for traders seeking high-risk, high-reward opportunities. This pair is influenced by both UK economic data and Japan’s monetary policy, making it highly responsive to geopolitical events.

- EUR/CHF: The Swiss franc is another safe-haven currency, and EUR/CHF is influenced by Swiss National Bank policies and Eurozone stability. This pair often reacts to global risk sentiment, with the Swiss franc strengthening during periods of market turbulence.

Correlation Between Cross Pairs and Major Pairs

One of the most practically important concepts for any trader active in cross currency pairs is understanding how those pairs correlate with the major pairs from which they are derived. Ignoring these correlations is one of the most common ways traders unknowingly double their exposure to a single currency without realizing it, which can produce unexpected losses when the market moves against them.

Because cross pairs are derived from major pairs through the USD as an intermediate currency, mathematical relationships exist between them that create predictable correlation patterns. Understanding these patterns is essential for proper portfolio construction and risk management.

| Cross Pair | Positive Correlation | Negative Correlation | Practical Implication |

| EUR/GBP | EUR/USD | GBP/USD | Long EUR/GBP + Long EUR/USD = double EUR exposure |

| EUR/JPY | EUR/USD, USD/JPY | Risk-off assets | Sensitive to both Eurozone data and global sentiment |

| GBP/JPY | GBP/USD, USD/JPY | Safe-haven flows | Among the most volatile due to dual correlation |

| EUR/CHF | EUR/USD | USD/CHF | Sensitive to Eurozone stability and Swiss National Bank policy |

Trading Strategies for Cross Currency Pairs

Trading cross currency pairs requires a tailored approach due to their unique characteristics. Unlike major pairs, which often follow clear USD-driven trends, cross pairs demand a deeper understanding of the economic fundamentals and technical patterns of the two currencies involved.

-

- Trend Analysis: Use tools like the 50-day and 200-day moving averages to identify long-term trends in cross currency pairs. For example, a crossover of these averages in EUR/GBP may signal a new trend. Additionally, pay attention to economic calendars for key data releases, such as GDP reports or employment figures, which can provide early signals of potential movements.

- Technical Indicators: Incorporate indicators like the Moving Average Convergence Divergence (MACD) or Bollinger Bands to spot entry and exit points. These tools help filter out market noise and highlight key support and resistance levels. For instance, a bullish MACD crossover in EUR/JPY could indicate a buying opportunity.

- Fundamental Analysis: Monitor economic indicators such as interest rate differentials, inflation rates, and political stability. For example, a rise in the UK’s interest rates may strengthen GBP/JPY, while political instability in the Eurozone could weaken EUR/CHF. Understanding these fundamentals is crucial for predicting volatility and making informed trading decisions.

Factors Affecting Cross Currency Pairs Prices

The price movements of cross currency pairs are influenced by a variety of factors, ranging from interest rate differentials to geopolitical events. Understanding these drivers is essential for predicting volatility and executing successful trades.

- Interest Rate Differentials: Higher interest rates in one currency relative to another can attract capital flows, strengthening that currency. For example, if the European Central Bank raises interest rates while the Bank of Japan keeps them low, EUR/JPY will likely rise as investors seek higher yields in the euro. Traders often use interest rate expectations as a leading indicator for potential pair movements.

- Political and Economic Stability: Events such as elections, referendums, or economic crises can cause significant volatility in cross currency pairs. For instance, political instability in the UK could weaken GBP/JPY, while economic reforms in Japan might strengthen the yen against the euro in EUR/JPY.

- Market Sentiment and Safe-Haven Flows: During periods of global uncertainty, safe-haven currencies like the Japanese yen or Swiss franc tend to strengthen. This can lead to significant movements in pairs such as EUR/JPY or GBP/CHF, as traders reposition their portfolios for safety. Monitoring market sentiment through tools like the Commitment of Traders (COT) report can provide valuable insights into these flows.

Trade Cross Currency Pairs With Confidence on Evest

Understanding cross currency pairs at this depth means you are ready for a trading environment that matches your level of analysis. Evest is a regulated, multi-award-winning CFD broker that gives you access to a full range of forex pairs, including the most actively traded cross pairs, with the execution quality, risk management tools, and platform flexibility that serious currency traders demand.

- Full access to major, minor, and cross currency pairs including EUR/GBP, EUR/JPY, GBP/JPY, AUD/JPY, EUR/CHF, and more

- Competitive spreads across all forex instruments with transparent pricing and no hidden fees

- MT5 platform with advanced charting, multi-timeframe analysis, and full indicator suite for session-based and correlation-aware trading

- Leverage of up to 1:400 on forex pairs, allowing precise position sizing across cross currency instruments

- Built-in stop loss and take profit tools for accurate risk management on pairs where pip values require currency conversion

- Islamic swap-free accounts available for eligible traders, removing overnight interest charges from carry trade calculations

- Web platform and mobile app for full trading flexibility across all global sessions from Asian open to New York close

- Regulated by VFSC Vanuatu and FSCA South Africa

- Awarded Best CFD Broker at Qatar Financial Expo & Awards QFEX 2025 and Best Trading Tools at Forex Expo Dubai 2024

Visit evest.com to open your account and access the full range of cross currency pairs with a broker built for informed traders.

FAQs

What is the difference between a cross currency pair and a major currency pair?

A cross currency pair involves two non-USD currencies, such as EUR/GBP, while a major pair includes the USD, like EUR/USD. Cross pairs are influenced by the economic relationship between the two currencies, whereas major pairs are directly tied to USD movements and global liquidity. This distinction means cross pairs often reflect regional economic trends more directly, offering unique trading opportunities.

Which cross currency pairs are the most liquid and why?

The most liquid cross currency pairs in 2026 include EUR/GBP, EUR/JPY, and GBP/JPY. Their liquidity stems from high trading volumes driven by strong economic ties between the involved regions. For example, EUR/GBP benefits from the proximity and economic integration of the Eurozone and the UK, while EUR/JPY is influenced by the Eurozone’s economic policies and Japan’s status as a haven.

How do interest rates impact the price of cross currency pairs?

Interest rates create differentials that attract or deter capital flows. For instance, if the ECB raises rates while the Bank of Japan maintains low rates, EUR/JPY will likely rise as investors seek higher yields in the euro. Conversely, if the Swiss National Bank raises rates, EUR/CHF may decline due to the increased attractiveness of the Swiss franc.

Can I trade cross currency pairs with the same strategies as major pairs?

While some strategies, such as technical analysis, apply to both cross and major pairs, cross currency pairs require additional focus on fundamental factors specific to the two currencies involved. For example, political events in the UK can significantly impact GBP/JPY but may not affect EUR/USD. Tailoring strategies to these unique drivers is key to success.

What are the best times of day to trade cross currency pairs for maximum volatility?

The best times to trade cross currency pairs are during the overlap of European and Asian trading sessions (7 AM to 12 PM GMT) or European and US sessions (8 AM to 12 PM GMT). These overlaps provide higher liquidity and volatility, especially for pairs like EUR/JPY, which are influenced by both Asian and European economic data releases.

How to Win the Trading Cup by Evest?

In the world of trading competition, winning never comes by chance — it comes through strategy, discipline, and the ability to make the right decision at the right moment. How to win the Trading Cup by Evest is the question on every serious trader’s mind who wants to see their name sitting at the top of the global leaderboard. The Cup doesn’t just reward whoever trades the most — it rewards whoever trades the smartest, and whoever understands how the ROI mechanism works and builds their plan around it from day one.

What Determines the Winner of the Trading Cup?

Before you put together a trading plan to win the Trading Cup, you need to understand the exact formula that determines your position on the leaderboard:

ROI (%) = ((Portfolio value at draw date − Deposits during campaign) ÷ Deposits during campaign) × 100

This means the competition isn’t about who generates the highest absolute return in dollars — it’s about who achieves the highest return rate relative to what they deposited. A trader who deposits $500 and achieves $1,000 in returns (200% ROI) outranks a trader who deposits $10,000 and achieves $1,500 (15% ROI). That’s the heart of the competition — and that’s exactly what makes the Cup fair for all participants regardless of account size.

What Do the Current Leaderboard Numbers Tell Us?

The current Draw 1 figures say everything — the top performer reached +1,599% and the second place +1,352%. These numbers don’t mean those traders took random risks. They mean they identified real opportunities in the market and capitalised on them using the trading tools available on the Evest platform.

Best Trading Competition Strategies for the Trading Cup

Strategies to win the Trading Cup differ from everyday trading strategies — because here you’re trading within a defined time window, with a clear goal, and an explicit performance formula. Here are the top approaches professional traders rely on:

1. Focus on High-Volatility Instruments

Instruments that move fast are the ones that create a real difference in return rates over short periods. On the Evest platform with 400+ financial instruments, you can choose from:

- Major currency pairs: EUR/USD, GBP/USD — directly impacted by major economic news

- Indices: S&P 500, NASDAQ — move sharply when US economic data is released

- Commodities: Gold and oil — among the most responsive instruments to geopolitical events

- Stocks: Clear opportunities around quarterly earnings reports

2. Smart Leverage Strategy

Evest offers leverage up to 1:400 on foreign currencies — an extremely powerful tool in a competitive context. Smart use of leverage means:

- Increasing position size to amplify potential returns

- Avoiding over-leveraging across multiple trades simultaneously

- Ensuring available margin protects you from a margin call before entering any position

3. News-Based Entry Strategy

Achieving the highest return in the Trading Cup is often tied to timing — and timing is tied to news. The economic calendar is your essential companion throughout the campaign period. Look out for:

- US Non-Farm Payrolls (NFP) — one of the most powerful monthly market movers

- Central bank interest rate decisions directly impact currencies and indices

- Inflation data (CPI) and growth indicators (GDP)

- Major corporate earnings reports — create sharp short-term movements in stocks

How to Top the Trading Cup Leaderboard — Practical Tips

Tips to win the Trading Cup go beyond technical strategy alone — they include mindset, planning, and time management throughout the competition window.

How to Top the Leaderboard — Step by Step?

- First — Start Early, Don’t Wait. The leaderboard updates in real time, and every day you delay is an opportunity your competitors are already capitalising on. Register your account, complete your KYC, and deposit as early as possible from the campaign start date.

- Second — Choose Your Financial Instrument Carefully. Don’t trade everything at once. Focus on the instruments you understand well and follow their news regularly — specialisation builds deeper confidence and sharper decision-making. One well-understood instrument consistently outperforms five half-understood ones.

- Third — Watch Your Competitors, Not Just the Market. The live leaderboard at champion evest shows you exactly where you stand relative to everyone else. Use that information to adjust your plan — if you’re in fifth place and targeting first, you need a higher return rate, not just maintaining your current level.

- Fourth — Don’t Open Random Trades Right Before the Draw Competition intensifies in the final days of each draw period, and that’s exactly when many traders make impulsive mistakes. Your decisions in the final hours must be analysis-driven — not pressure-driven. The draw date is a deadline, not a trigger for panic trading.

Risk Management in the Trading Cup — The Real Weapon of Champions

The best way to win the Trading Cup doesn’t mean taking maximum risk — it means applying risk management in the Trading Cup with the intelligence that keeps your capital alive and active through to the very last moment of each draw period.

Risk Management Tools on the Evest Platform

Evest provides a complete toolkit for protecting your capital:

- Stop Loss: Define your maximum acceptable loss per trade upfront — never leave a position open without a ceiling

- Take Profit: Set your target before entering the trade, and don’t let greed give back what you’ve already achieved

- Pending Orders: Enter the market at the price you want rather than the live price — especially when anticipating strong movements

- Capital Distribution: Never put all your capital into a single position — diversification reduces risk and keeps you in the game longer

The Golden Rule in Trading Competitions

Skills to win a trading challenge are not measured solely by the size of the return you achieve — they’re measured by your ability to protect what you’ve built all the way to the draw date. A trader who achieves +300% then loses half of it before the draw ends at +150% — while the patient, disciplined trader who manages their risk properly, takes the lead by a wide margin.

Why Evest Is the Ideal Platform to Win the Trading Cup

The best trading competition strategies are incomplete without a powerful trading platform backing every move. Evest doesn’t just host a tournament — it delivers a complete trading environment that gives you every tool you need to compete at the highest level:

- 0.03ms order execution — never miss a market opportunity due to execution delay

- Trading Central — technically-driven recommendations from a licensed third-party provider to sharpen your decisions

- TipRanks — an AI-powered stock analysis tool to understand market trends at a deeper level

- Trading Academy — comprehensive educational content from beginner to professional.

- Expert Webinars with Ahmed Osama — exclusive market analysis sessions with Evest’s lead analyst for exceptional market insight

- Copy Trading — study the patterns of top traders to develop and refine your own strategy.

CFD trading involves significant risk. Your capital is at risk. Make sure you fully understand the risks before you start trading.

FAQs

Can a beginner win the Trading Cup?

Yes — and the leaderboard numbers prove it. The ROI formula levels the playing field regardless of account size. A beginner trader with $500 can achieve a return rate that outperforms a professional with $50,000, as long as they make the right decisions at the right time. The key is focusing on one or two instruments you understand well and using the analytical tools available on the Evest platform to make informed decisions rather than random ones. How to win a trading competition as a beginner comes down to focus, not size.

How do I choose the right financial instrument for the Trading Cup?

Choosing your instrument is one of the most important decisions in finding the best way to win the Trading Cup. High-volatility instruments such as major currency pairs, gold, and US indices allow for significant price movements over short time periods, making them well-suited for weekly competition windows. Use the Trading Central tool available on the Evest platform to get specific technical recommendations, and follow the economic calendar to know exactly when high-impact news events are scheduled before making any entry decision.

Does risk management slow down achieving the highest return in the Cup?

This is a question many traders ask, and the direct answer is: no. Risk management in the Trading Cup is not an obstacle — it's what keeps you in the competition. Winning isn't about achieving the highest return in a single day then giving it back before the draw date. It's about maintaining a strong, stable return rate all the way to the moment results are calculated. Place a Stop Loss on every trade, distribute your capital across more than one opportunity, and always remember — the goal is to win the draw, not just to feel the rush of a big single-day move.

What Is the Difference Between SPX vs SPXW Options?

Understanding the distinction between SPX vs SPXW options is crucial for traders aiming to optimize their strategy. Both track the S&P 500 Index, but their settlement mechanics, expiration cycles, and tax implications create unique opportunities. Whether you’re a short-term volatility trader or a long-term investor, mastering these differences can significantly enhance your options trading performance. This guide explores the core distinctions, settlement processes, tax treatments, and strategic applications of SPX and SPXW options to help you make informed decisions.

SPX vs SPXW Options: Core Differences

| Point | SPX Options | SPXW Options |

| Contract Type | SPX options are standard monthly contracts tied to the S&P 500 Index. They are commonly used for longer-term index exposure and have been part of index options trading since the 1980s. | SPXW options are weekly contracts designed for short-term trading strategies. They are mainly used by traders who want to benefit from intraday or weekly market volatility. |

| Expiration Cycle | SPX options typically expire on the third Friday of each month, offering a more predictable monthly expiration structure. | SPXW options usually expire every Friday, giving traders more frequent opportunities to adjust positions based on market movements. |

| Trading Use | SPX options are often preferred by investors and traders with a longer time horizon who want more stability and structured exposure to the S&P 500 Index. | SPXW options are commonly used for weekly options strategies, short-term positioning, and daily or near-term expiration trading. |

| Underlying Index | Both SPX and SPXW options derive their value from the same underlying S&P 500 Index. | Both contracts track the same S&P 500 Index, but SPXW options differ mainly in their shorter expiration cycles and trading flexibility. |

| Availability | SPX options follow the standard monthly options schedule. | SPXW options are not available every day; they follow a structured weekly schedule aligned with broader options market trading days. |

| Liquidity and Strategy | SPX options may suit traders looking for more established monthly contracts and longer-term positioning. | SPXW options can support active trading strategies, but traders should still monitor liquidity, volatility, and expiration risk carefully. |

SPX vs SPXW Settlement: How They Work

- SPX options utilize AM settlement, where the final index value is determined before the market opens. This method provides a stable reference point for overnight positions but limits the ability to react to late-day market shifts.

- SPXW options employ PM settlement, calculating the final index value at the close of trading. This approach benefits traders who rely on intraday momentum or news-driven moves, as it captures the full day’s price action.

- The difference in settlement timing can significantly impact profit calculations. For example, a trader holding a SPXW call option may experience substantial gains if the index rallies sharply in the final hour, whereas the same move in a SPX call would only reflect the following morning.

- Edge cases, such as holidays or early exercise, further highlight the importance of understanding settlement mechanics. SPXW options cannot be exercised early, unlike SPX options, which adds another layer of strategy for traders managing risk in options trading.

The Greeks in SPX vs SPXW: Why They Behave Differently

Understanding how SPX and SPXW options are priced on the surface is only part of the picture. The real edge comes from understanding how the Greeks behave differently across the two contract types, particularly as expiration approaches. This distinction becomes especially critical for traders using 0DTE strategies on SPXW options, where Greek sensitivity accelerates at a pace that catches unprepared traders off guard.

Gamma and Theta: The 0DTE Dynamic

Gamma, which measures how quickly Delta changes as the underlying index moves, reaches its most extreme values in the final hours of a SPXW 0DTE contract. This means that a relatively small move in the S&P 500 Index can produce an outsized and rapidly changing profit or loss on a short-dated SPXW position. Theta, the rate at which an option loses value due to time decay, works in parallel, accelerating dramatically in the final session of a SPXW expiration. For SPX monthly options, these same Greek forces are present but spread across a much longer time horizon, making them far more manageable for traders who prefer gradual position monitoring.

The practical implication is straightforward. SPXW 0DTE traders are effectively managing a position where the rules of the game are changing by the minute, while SPX monthly traders operate in a slower-moving environment where adjustments can be planned over days rather than hours. Neither approach is superior, but each demands a completely different risk management mindset and a clear understanding of Greek behavior at the relevant time to expiration.

SPX vs SPXW Expiration: Weekly vs Monthly Cycles

- SPX options expire monthly, typically on the third Friday of each month, aligning with the standard options market cycle. This predictability makes them suitable for long-term strategies and hedging.

- SPXW options expire weekly, every Friday, offering traders the flexibility to reset positions more frequently. This cycle is particularly advantageous for short-term traders focusing on volatility trading and weekly options.

- The 60/40 tax rule applies to SPXW options expiring between 30 and 60 days, where 60% of gains are taxed as long-term capital gains and 40% as short-term. This can provide significant tax advantages for traders in 2026.

- Comparing SPX and SPXW options expiring on the same day reveals how settlement and expiration mechanics influence returns. SPXW options often yield higher profits in volatile markets due to their shorter time decay and PM settlement, while SPX options offer stability for longer-term holds.

Tax Treatment: SPX vs SPXW Options

- SPX options may qualify for long-term capital gains treatment due to their monthly expiration cycle, reducing tax burdens for investors holding positions beyond one year.

- SPXW options are typically taxed as short-term gains because of their weekly expirations, but they may qualify for Section 1256 tax treatment if held for more than a year or used in hedging strategies. This treatment can lower tax obligations by averaging gains over time.

- Mark-to-market rules at year-end require traders to recognize gains and losses annually for SPXW options held until December 31. This can lead to unexpected tax liabilities if the market moves unfavorably.

- Short-term traders benefit from the 60/40 rule when trading SPXW options, while long-term investors leverage the lower capital gains rates associated with SPX options. Understanding these nuances is essential for optimizing tax efficiency in derivatives trading.

VIX and Volatility Pricing: How SPX and SPXW Options React Differently

The VIX, commonly known as the market’s fear gauge, measures the implied volatility of S&P 500 Index options over 30 days. While both SPX and SPXW options derive their value from the same underlying index, their sensitivity to VIX moves and implied volatility shifts is meaningfully different, and understanding this distinction can significantly affect how you price, sell, or buy these contracts.

How Implied Volatility Affects Each Contract Type?

SPX monthly options are more directly influenced by the 30-day implied volatility window that the VIX measures. When the VIX spikes due to a macro event or market shock, the premium in SPX monthly options expands substantially, which benefits sellers of those options but increases the cost for buyers. SPXW weekly options, with their much shorter time to expiration, respond to implied volatility in a more compressed and often more volatile way. A VIX spike that might add meaningful premium to a monthly SPX contract can cause disproportionately large moves in the pricing of an SPXW weekly that expires within days.

This difference matters most during earnings seasons, Federal Reserve announcements, and geopolitical events. Traders who understand that short-dated SPXW options can experience extreme implied volatility expansion and contraction around these events are far better positioned to avoid the twin dangers of overpaying for protection or selling premium at the worst possible time. Monitoring implied volatility rank and percentile for both contract types before entering any position is an essential step that the settlement mechanics discussion alone cannot replace.

Liquidity and Bid-Ask Spreads: The Hidden Cost Difference

One of the most practically significant differences between SPX and SPXW options that often goes unexamined in introductory comparisons is the difference in liquidity profiles and their direct impact on execution costs. Liquidity in options markets is not uniform across strikes, expiration dates, or contract types, and the gap between the bid and ask price represents a real cost that compounds across multiple trades.

SPX monthly options, particularly at near-the-money strikes in the front month, tend to carry very tight bid-ask spreads due to the concentration of market maker activity and trader interest around those contracts. SPXW weekly options can be highly liquid at near-the-money strikes in the expiring week but may show wider spreads at further out-of-the-money strikes or at weekly expirations that are less actively traded.

What This Means for Your Actual Trading Costs

Consider the following practical comparison between the two contract types from a cost perspective.

| Cost Factor | SPX Monthly Options | SPXW Weekly Options |

| Bid-Ask Spread at ATM | Generally tighter | Can widen near expiration |

| Liquidity at OTM Strikes | Deep and consistent | Varies by week and strike |

| Market Impact of Large Orders | Lower for monthly contracts | Higher for weekly OTM strikes |

| Cost Per Round Trip | Lower on liquid monthly strikes | Higher on less active weeklies |

The implication for active traders is that the frequency advantage of SPXW weeklies, which allows you to reset positions every Friday, comes with a potential cost disadvantage in terms of wider spreads on less liquid strikes. Calculating your all-in cost per trade, including the bid-ask spread, is as important as evaluating the strategy itself when deciding between SPX and SPXW contracts.

Trading Strategies: Which to Choose for Your Style?

- SPX Weeklys are ideal for credit spreads and iron condors, where traders profit from time decay and limited market movement. These strategies are well-suited for active traders focusing on volatility trading.

- SPX monthly options are better for long-term directional bets or hedging strategies, providing stability and alignment with broader market trends.

- 0DTE (zero days to expiration) day trading is a high-risk, high-reward strategy that thrives with SPXW options due to their PM settlement and weekly cycle. Traders must manage rapid time decay and gamma risk carefully.

- Risk management is critical when trading SPXW options. Position sizing, stop losses, and delta-neutral strategies help mitigate losses in fast-moving markets.

Trade the S&P 500 Your Way With Evest

Whether you are analyzing SPX settlement mechanics, managing Greek exposure on short-dated contracts, or monitoring VIX-driven premium shifts, having the right trading infrastructure behind you makes every difference. Evest is a regulated CFD trading platform that gives you direct access to major global indices, including the S&P 500, with the tools and execution environment that serious traders require.

Here is what Evest offers traders focused on index markets:

- CFD trading on major global indices, including the S&P 500, with competitive spreads

- Real-time pricing and execution across the web platform, mobile app, and MT5

- Leverage options available on index CFDs for amplified market exposure

- Built-in stop loss and take profit tools for precise risk management around key levels and expiration windows

- Zero-commission trading on stock CFDs alongside your index positions

- Islamic swap-free accounts available for eligible traders

- Regulated by VFSC Vanuatu and FSCA South Africa for a secure trading environment

- Awarded Best CFD Broker at Qatar Financial Expo & Awards QFEX 2025 and Best Trading Tools at Forex Expo Dubai 2024

Visit evest.com to open your account and access global index markets with a broker built for the informed trader.

FAQs

What is the difference between SPX and SPXW options expiring on the same day?

SPX options settle in the AM based on the open, while SPXW options settle in the PM based on the close. This means SPXW options capture intraday moves that SPX options miss. Additionally, SPXW options expire weekly, offering more frequent trading opportunities compared to SPX’s monthly cycle.

Do SPXW options qualify for Section 1256 tax treatment, and how does this affect trading?

SPXW options may qualify for Section 1256 tax treatment if held for over a year or used in hedging. This reduces tax burdens by allowing 60% of gains to be taxed as long-term capital gains. Most traders use SPXW for short-term plays, but strategic positions can benefit from this rule.

Can SPXW options be exercised early, and how does this differ from SPX options?